Medicare Supplement insurance — also called Medigap — fills the gaps that Original Medicare leaves behind. When Medicare pays its share of a covered service, your Medigap plan picks up costs like your 20% coinsurance, hospital deductibles, and copays. The result: very predictable healthcare costs and the freedom to see any Medicare-accepting doctor in the country, no network required.

If you’ve heard Medicare Advantage described as the “cheaper” option, keep reading. I’m going to walk you through exactly how Medigap works, when it makes more sense than Medicare Advantage, and what to watch out for. No sales pitch — just the truth as I’d tell it across the table from you.

What Is Medigap (Medicare Supplement Insurance)?

Original Medicare covers a lot — but it doesn’t cover everything. It pays 80% of most Part B services, leaving you responsible for the other 20% with no annual cap on that exposure. If you have a serious health event — surgery, hospitalization, chemotherapy — that 20% can add up to tens of thousands of dollars.

Medigap is private insurance designed specifically to cover those leftover costs. You keep Original Medicare as your primary coverage. Medigap pays second. Together, they act like a wall between you and unpredictable medical bills.

How Does Medigap Differ From Medicare Advantage?

This is the decision most people turning 65 face. They’re fundamentally different approaches to Medicare coverage:

| Feature | Medigap + Original Medicare | Medicare Advantage (Part C) |

|---|---|---|

| Monthly premium | $100–$300+/mo (varies by plan and age) | $0–$100+/mo (plus $202.90 Part B) |

| Provider choice | Any Medicare-accepting doctor nationwide | Typically network-restricted (HMO/PPO) |

| Out-of-pocket costs | Very predictable — Medigap covers most gaps | Variable — depends on services used |

| Annual out-of-pocket max | Near zero once you hit your Medigap coverage | Up to $9,350 in-network (2026) |

| Prior authorization | Rarely required | Common — insurer must approve many services |

| Prescription drugs | Separate Part D plan required | Usually included in plan |

| Dental/Vision/Hearing | Not included — separate coverage needed | Often included |

| Travel / out-of-state | Works anywhere Medicare is accepted | Network may not cover out-of-state care |

Neither is automatically better. Medicare Advantage tends to work well for healthy people on tight budgets who stay in one area. Medigap tends to work better for people with ongoing health needs, frequent travelers, or anyone who values predictability and unlimited provider choice.

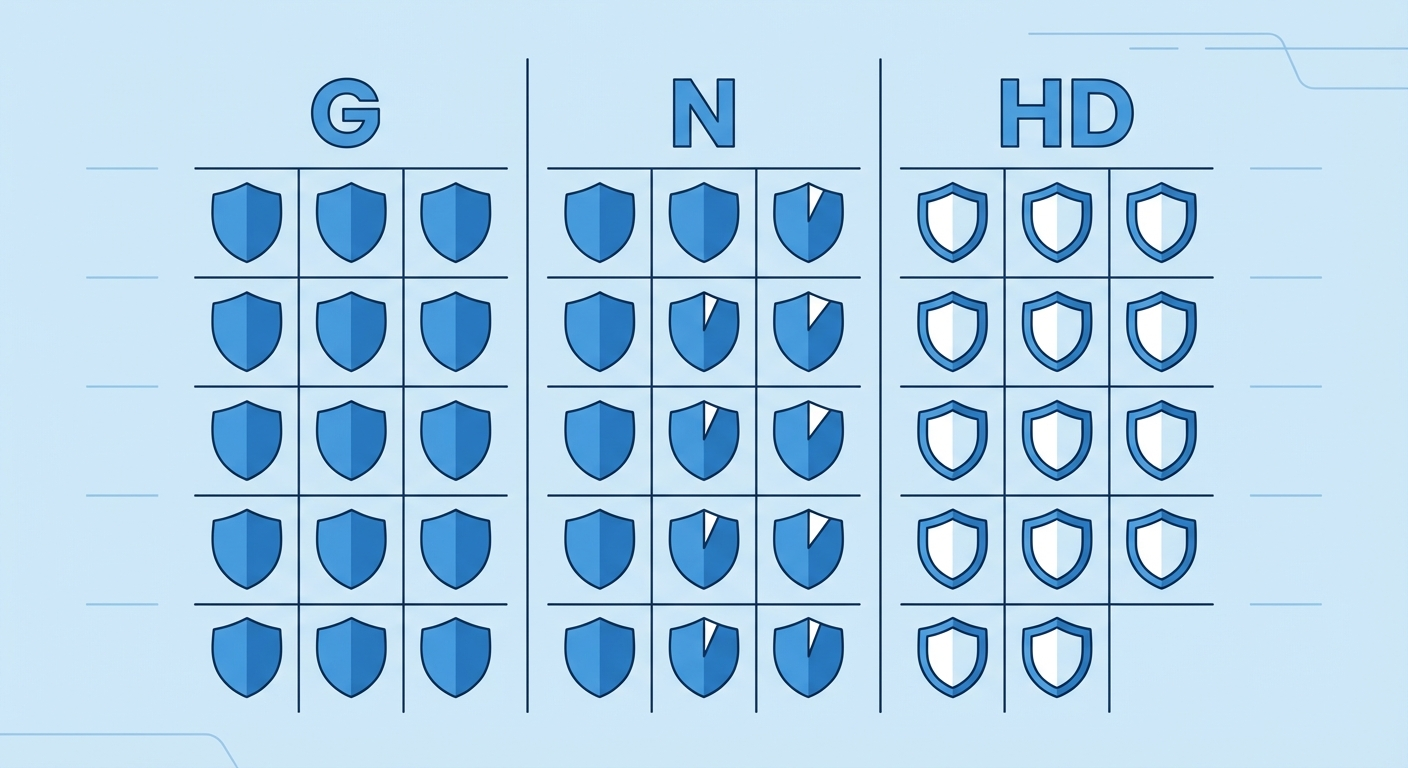

Medigap Plan Types — What Each One Covers

Medigap plans are standardized by the federal government — that means a Plan G from one company covers exactly the same things as a Plan G from another company. The only difference is the premium. Here are the most common plans:

| Plan | Part A Coinsurance | Part B Coinsurance | Part A Deductible | Part B Deductible | Foreign Travel | Best For |

|---|---|---|---|---|---|---|

| Plan G ⭐ Most popular | ✅ | ✅ | ✅ | ❌ (you pay $257/yr) | ✅ 80% | Most new enrollees — best coverage after Plan F |

| Plan N | ✅ | ✅ (with copays) | ✅ | ❌ | ✅ 80% | Healthy, cost-conscious enrollees OK with small copays |

| Plan F (pre-2020 only) | ✅ | ✅ | ✅ | ✅ | ✅ 80% | Those enrolled before Jan 1, 2020 only |

| Plan K / L | Partial | Partial | Partial | ❌ | ❌ | Lower premium, higher cost-sharing tolerance |

For most people enrolling today, Plan G is the sweet spot. It covers nearly everything except the Part B deductible ($257 in 2026), and the premium savings over Plan F usually more than offset that deductible. Plan N is a good second option for healthy enrollees willing to pay small copays in exchange for lower monthly premiums.

How Much Does Medigap Cost?

Medigap premiums vary based on your age, gender, location, tobacco use, and which company you choose. For a typical 65-year-old non-smoker, here’s a rough range:

- Plan G: $100–$200/mo at age 65 (increases as you age)

- Plan N: $80–$160/mo at age 65

- Plan F: $150–$250/mo (only available to pre-2020 enrollees)

Add your Part B premium ($202.90/mo in 2026) and a Part D drug plan ($20–$60/mo) on top of your Medigap premium for your total monthly healthcare spend. That said, your out-of-pocket costs for actual care are very low — which is the trade-off you’re making.

I find that a lot of people look at the higher Medigap premium and assume Medicare Advantage is cheaper. Sometimes it is — if you’re healthy and rarely use care. But if you have ongoing health needs, the math often flips. That’s why I run the actual numbers for you based on your specific situation.

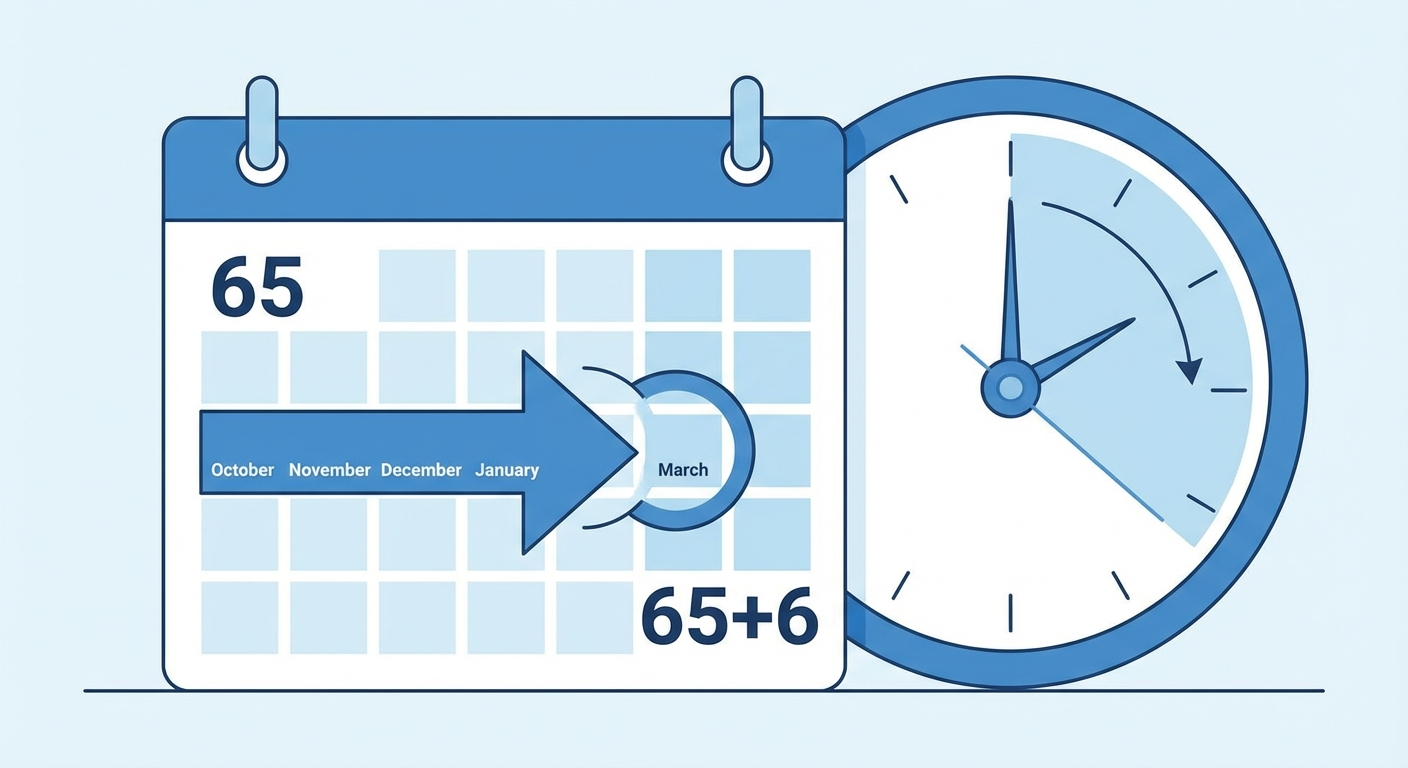

When Can You Enroll in Medigap?

This is the most important thing to understand about Medigap — and the thing most people don’t know until it’s too late.

Your Open Enrollment Window — Use It

When you first enroll in Medicare Part B, you have a 6-month Medigap Open Enrollment Period. During this window, insurers cannot deny you coverage or charge you more based on your health. You have guaranteed issue rights — you can get any Medigap plan sold in your state regardless of your health history.

This window does not repeat. Once it closes, insurers in most states can use medical underwriting — meaning they can deny you coverage or charge significantly higher premiums based on your health conditions.

The Switch-Back Problem With Medicare Advantage

Here’s the scenario I see too often: someone chooses a Medicare Advantage plan at 65, develops a serious health condition at 70, and then wants to switch to Medigap for better coverage. In most states, they can’t — or they can only get limited plans because they no longer have guaranteed issue rights. Their health history now works against them.

This doesn’t mean Medicare Advantage is wrong for everyone. But it’s a risk you need to understand before you make your initial Medicare decision — not after you’ve been on an MA plan for five years.

Who Is Medigap the Right Choice For?

✅ Medigap Tends to Work Well For…

- People with ongoing health needs or chronic conditions

- Frequent travelers or those who split time between states

- Anyone who wants to keep their current doctors without network concerns

- People who value predictable, stable monthly costs

- Those who want maximum flexibility in choosing specialists

⚠️ Medigap May Not Be the Best Fit If…

- You’re on a tight fixed income and the higher premium is genuinely unaffordable

- You’re very healthy and rarely use medical services

- You want dental, vision, and hearing included in one plan

- Your doctors are all in-network for a local Medicare Advantage plan

Does Medigap Cover Prescription Drugs?

No. Medigap plans do not include prescription drug coverage. If you’re on a Medigap plan, you’ll need a separate Medicare Part D drug plan to cover your prescriptions. Part D plans are sold by private insurers and vary in cost and formulary — running roughly $20–$60/month for most enrollees depending on your medications.

Don’t skip Part D just because you’re not on medications today. If you delay enrollment past your initial window, you face a permanent late enrollment penalty for every month you went without coverage.

How to Choose the Right Medigap Plan

- Start during your Open Enrollment window — You have guaranteed issue rights. Don’t wait until your health changes.

- Compare Plan G vs. Plan N — Plan G covers almost everything. Plan N costs less but has small copays. For most people, one of these two is the right answer.

- Compare premiums across carriers — Same plan, different companies, very different prices. An independent broker does this comparison for you at no cost.

- Factor in Part D — Run your prescription drug list through plan formularies to find the best match.

- Think long-term — Premiums increase as you age. Some companies raise rates faster than others. Carrier stability matters.

Frequently Asked Questions

What is Medigap and how does it work?

Medigap is private insurance that supplements Original Medicare. When Medicare pays its share of a covered service, your Medigap plan picks up costs like your 20% coinsurance and hospital deductibles. You pay a monthly premium to the Medigap insurer; they handle the rest automatically.

What is the best Medigap plan in 2026?

For most people enrolling today, Plan G is the best value. It covers nearly everything except the Part B deductible ($257 in 2026). Plan N is a strong alternative for healthy enrollees comfortable with small copays in exchange for lower monthly premiums.

How much does Medigap cost per month?

Premiums vary by plan, age, gender, and location. A typical 65-year-old non-smoker pays $100–$200/month for Plan G, plus the $202.90 Part B premium and a separate Part D drug plan. Total monthly healthcare spend is typically $250–$400+ depending on plan and location.

Can I be denied Medigap coverage?

During your 6-month Open Enrollment Period (when you first enroll in Part B), insurers cannot deny you or charge more based on health. After that window, most states allow medical underwriting — meaning pre-existing conditions can result in denial or higher premiums. Enrolling during your open enrollment window is critical.

Does Medigap cover dental and vision?

No. Medigap covers the gaps in Original Medicare — hospital, medical, and outpatient costs. It does not include dental, vision, or hearing. You’d need separate standalone plans for those. This is one area where Medicare Advantage often has an advantage for enrollees who want everything bundled.

Can I switch from Medicare Advantage to Medigap?

Yes, technically — during the Annual Enrollment Period or MA Open Enrollment Period. But if you’ve developed health conditions while on a Medicare Advantage plan, most states allow Medigap insurers to deny you coverage or charge more based on your health history. This is why the initial Medicare decision matters so much. It’s worth thinking through before you choose, not after.

Explore Your Other Medicare Options

Medicare Overview

New to Medicare? Start here — Parts A, B, C, D explained in plain English. Enrollment windows, penalties, and the route decision.

Medicare Advantage

The alternative to Original Medicare + Medigap. Often $0 premium with dental, vision, and prescriptions bundled. Here’s what the commercials don’t tell you.

Life Insurance

Protect your spouse’s income and financial security in retirement. Final expense and term options — no pushy sales.

Ready to Compare Medigap Plans?

I compare Medigap plans across multiple carriers — same coverage, different prices. You deserve to know all your options before you choose. And it costs you nothing to work with me.

No pressure. No one-carrier agenda. Just a clear, honest look at what’s available in your area.

Or call me directly. I answer my own phone.

Have questions about Medigap before booking? Speak with an advisor — free consultation, no commitment required.

Marc is a licensed independent Medicare insurance broker serving clients in Colorado and other states. Plan availability, benefits, and costs vary by location. This page is for educational purposes and does not constitute enrollment advice. Coverage decisions should be based on your individual situation. Medigap benefits and premiums vary by insurer and state. Data referenced reflects 2026 CMS guidelines.